In 2025, the smartest investors do not sell their Bitcoin. Selling is a taxable event. Selling forfeits future upside. Selling is what the middle class does.

The wealthy do something else: They borrow against their assets.

Real estate tycoons have done this for decades (refinancing properties). Now, cryptocurrency allows anyone to do the same instantly, without a credit check, and often with lower interest rates than a credit card.

Whether you need $10,000 for a home renovation or $1,000,000 to buy a business, Crypto Lending allows you to unlock the liquidity of your portfolio while maintaining ownership of your coins.

This guide will dissect the lending landscape of 2025. We will compare CeFi (Centralized) platforms like Nexo and Ledn against DeFi (Decentralized) protocols like Aave, helping you navigate the risks of "Rehypothecation" and "Liquidation" to access capital safely.

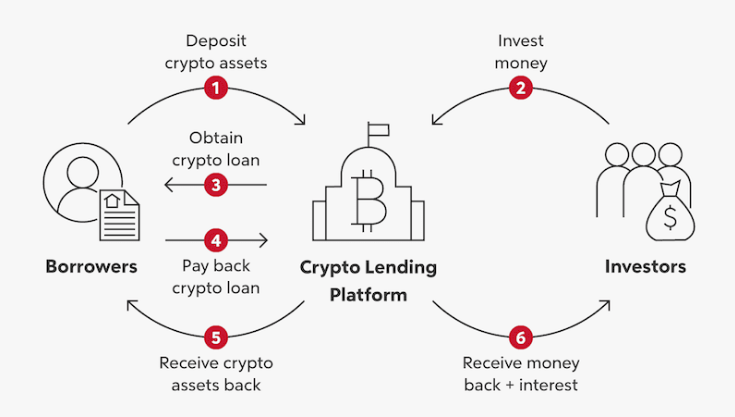

Part 1: The Mechanics of a Crypto Loan

Unlike a bank loan, crypto loans are Over-Collateralized. You don't need a credit score; you need collateral.

The Formula: Loan-To-Value (LTV)

This is the most critical metric.

-

Equation: LTV = (Loan Amount / Collateral Value) * 100.

-

Example: You have $10,000 worth of Bitcoin. You want to borrow $5,000 cash (USDC or USD).

-

Your LTV: ($5,000 / $10,000) * 100 = 50%.

The Rules of the Game

-

Low LTV (Safe): If you borrow at 20% LTV, Bitcoin price must drop 80% before you are in trouble.

-

High LTV (Risky): If you borrow at 80% LTV, a 10% drop in Bitcoin price triggers a liquidation.

-

Liquidation: If the value of your collateral drops too low, the lender automatically sells your Bitcoin to pay off the loan. You keep the cash, but lose the Bitcoin.

Part 2: The "Tax Hack" Strategy (Buy, Borrow, Die)

Why borrow at 5% interest? To save 20%+ in taxes.

Scenario A: The Seller

-

You bought 1 BTC at $10,000. It is now $100,000.

-

You sell $50,000 worth to buy a car.

-

Tax Bill: You owe Capital Gains Tax on the $45,000 profit. (Approx $9,000 tax).

-

Asset Status: You have 0.5 BTC left.

Scenario B: The Borrower

-

You deposit 1 BTC ($100,000) as collateral.

-

You borrow $50,000 cash.

-

Tax Bill: $0. (Loans are not income; they are debt).

-

Asset Status: You still own 1 BTC. If BTC goes to $200,000, you capture all that upside.

-

Cost: You pay ~5% interest per year ($2,500).

-

Victory: Buying the car cost you $2,500 in interest instead of $9,000 in taxes, AND you still own the Bitcoin.

Part 3: Top Crypto Lending Platforms 2025 (CeFi vs DeFi)

The market has consolidated after the 2022 crashes (Celsius, BlockFi). The survivors are stronger, regulated, and more transparent.

1. Nexo: The User-Friendly Giant

Verdict: Best for daily spending and credit lines.

-

Overview: Nexo operates like a modern bank. They have serviced over 6 million users.

-

Product: Instant Crypto Credit Line. You can spend cash via the Nexo Card without selling your crypto.

-

Interest Rates: Borrowing starts at 0% (if LTV is <20%) up to 13.9%.

-

Security: Real-time auditing by Armanino to prove reserves.

-

Pros: Extremely polished app. The credit card allows you to spend "credit" backed by your crypto seamlessly at Starbucks.

2. Ledn: The Bitcoin-Only Fortress

Verdict: Best for safety-first Bitcoiners.

-

Overview: Ledn (based in Canada) focuses purely on Bitcoin and USDC. They shun altcoins to minimize risk.

-

Key Feature: Proof of Reserves. Ledn was the first lender to publish a client-specific proof of reserves, showing exactly where your assets are.

-

Loan Type: "Standard Loan" (Rehypothecated - lower rate) vs. "Custodied Loan" (Assets sit in a vault and are never touched - higher rate).

-

Pros: Transparency is unmatched. No native token to manipulate.

3. Aave (DeFi): The Trustless Option

Verdict: Best for those who don't want KYC.

-

Overview: Aave is a decentralized protocol running on Ethereum. No company controls it.

-

Process: You deposit WBTC (Wrapped Bitcoin) into a smart contract and borrow USDC instantly.

-

Pros: No credit check, no KYC, no human can reject your loan.

-

Cons: Interest rates fluctuate every second based on supply/demand. Smart contract risk exists.

4. YouHodler: The High LTV Specialist

Verdict: Best for aggressive traders.

-

Overview: A Swiss-based platform known for offering high LTV limits (up to 90%).

-

Feature: Multi HODL. A tool that automates the "Looping" strategy to short/long the market using borrowed funds.

-

Pros: Regulated in Switzerland and Italy. Very responsive support.

Part 4: Comparative Analysis Table

|

Feature |

Nexo |

Ledn |

Aave (DeFi) |

YouHodler |

|---|---|---|---|---|

|

Type |

CeFi (Company) |

CeFi (Company) |

DeFi (Protocol) |

CeFi (Company) |

|

KYC Required |

Yes |

Yes |

No |

Yes |

|

Min. Loan |

$50 |

$500 |

$0 |

$100 |

|

LTV Limit |

Up to 50% |

Up to 50% |

Up to 75% |

Up to 90% |

|

APR (Interest) |

0% - 13.9% |

~12% |

Variable (2% - 20%) |

~13% |

|

Collateral |

BTC, ETH, Altcoins |

BTC Only |

ERC-20 Tokens |

50+ Coins |

|

Safety |

High (Real-time Audit) |

Very High (PoR) |

Code Dependent |

High (Swiss Reg) |

Part 5: The Risks (The Ghost of Celsius)

We cannot talk about lending without addressing the elephant in the room: Platform Bankruptcy.

1. Rehypothecation Risk

-

What is it? When you deposit Bitcoin to borrow cash, the lender doesn't just put your Bitcoin in a vault. They lend it out to institutions (like hedge funds) to earn yield.

-

The Danger: If the hedge fund defaults (like Three Arrows Capital did), the lender might lose your collateral.

-

The Solution: Use Ledn's "Custodied Loans" where they legally promise not to touch your collateral (you pay a higher rate for this safety). Or use DeFi (Aave) where collateral stays in a contract.

2. Margin Call / Liquidation

-

Scenario: You borrow $50,000 against $100,000 BTC (50% LTV).

-

The Crash: BTC drops to $60,000. Your LTV is now 83%.

-

The Call: The platform emails you: "Deposit more BTC now or we sell."

-

The Mitigation: Never borrow more than 25-30% LTV. If BTC drops 50%, you are still safe.

3. Smart Contract Risk (DeFi Only)

-

Risk: A bug in Aave's code allows a hacker to drain the collateral pool.

-

Mitigation: Purchase insurance via protocols like Nexus Mutual.

Part 6: Step-by-Step Guide: Getting a Loan on Ledn

For maximum safety, we will walk through a Ledn loan process.

-

Account Setup: Register and complete KYC (Passport/ID).

-

Deposit: Send Bitcoin to your Ledn Wallet. Wait for 3 confirmations.

-

Application: Click "Borrow."

-

Select "Standard" or "Custodied."

-

Input amount (e.g., 5,000 USDC).

-

Review LTV (Ensure it is <50%).

-

-

Approval: Automated. Usually takes less than 24 hours to fund.

-

Funding: You receive USDC in your Ledn wallet.

-

Withdraw: Send that USDC to your bank account (via Coinbase) or spend it.

-

Repayment: You can pay monthly interest only, and pay the principal whenever you want. There is no fixed deadline.

Conclusion: Leverage is a Double-Edged Sword

Crypto lending is the most powerful tool for wealth preservation in the 21st century. It breaks the cycle of "Selling assets to pay for life."

-

Use it to: Buy real estate, pay off high-interest credit cards, or delay taxes.

-

Do NOT use it to: Buy a Lamborghini or "Ape" into memecoins.

If you treat your Bitcoin as Primal Collateral—never to be sold, only borrowed against—you have unlocked the secret of dynastic wealth. Choose your platform wisely, keep your LTV low, and let your assets work for you.

FAQ: Frequently Asked Questions

Q1: What happens if Bitcoin price goes up? Great news! Your LTV drops. You can essentially "refinance" to borrow more money without adding collateral, or withdraw some of your Bitcoin back to your wallet.

Q2: Do I lose ownership of my crypto? Technically, in CeFi, you transfer title to the lender for the duration of the loan. In DeFi, you retain ownership via the smart contract. In both cases, you cannot trade or move the locked collateral.

Q3: Can I pay off the loan early? Yes. Most top platforms (Nexo, Ledn) have no prepayment penalties. You can pay off the loan 1 day after taking it.

Q4: Is interest paid on crypto loans tax-deductible? It depends on your jurisdiction and the purpose of the loan. In the US, if you use the loan proceeds to buy investments (like stocks or real estate), the interest may be deductible as "Investment Interest Expense." Consult a CPA.

Q5: Which is safer: Nexo or Aave?

-

Nexo is safer against "User Error" (you can call support if you lose your password).

-

Aave is safer against "Corporate Bankruptcy" (no CEO to run away with funds). Pick your poison based on your technical comfort level.